Navigating Medicare Supplement Plan F with AARP

Are you approaching Medicare eligibility and feeling overwhelmed by the supplemental insurance options? Choosing the right coverage is a crucial decision for your future healthcare needs. This comprehensive guide dives deep into the now-discontinued Medicare Supplement Plan F offered through AARP, providing valuable insights to help you navigate the landscape of Medicare supplemental insurance even though Plan F is no longer available to new enrollees.

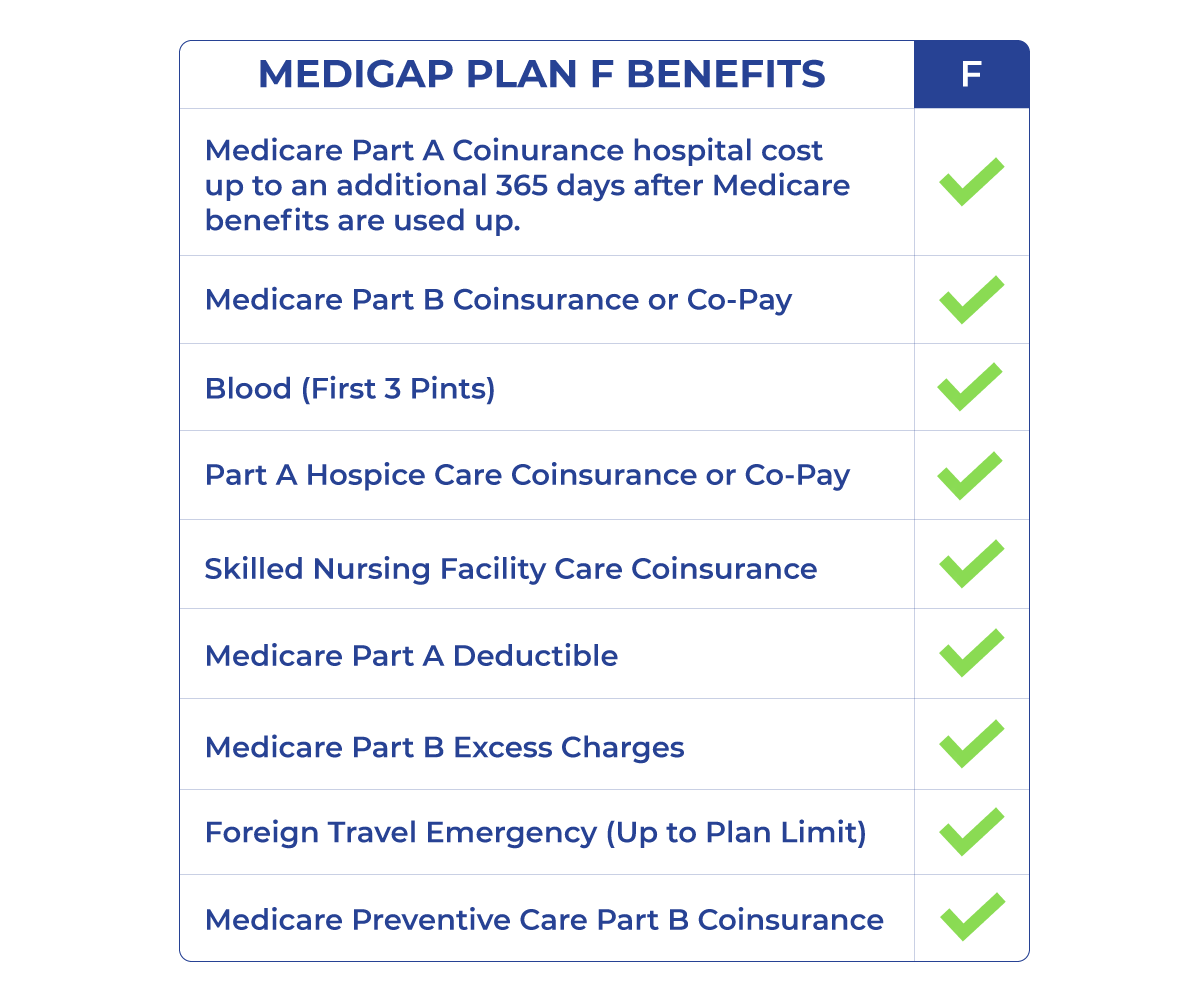

Medicare Supplement Plan F, often referred to as Medigap Plan F, was designed to fill the gaps in Original Medicare (Parts A and B) coverage. For those enrolled before January 1, 2020, it provided comprehensive protection against out-of-pocket costs like copayments, coinsurance, and deductibles. While AARP doesn't directly underwrite insurance, they endorse plans from UnitedHealthcare, making them a popular choice for seniors seeking reliable coverage.

Understanding the intricacies of Medigap plans, particularly those like Plan F, is essential for maximizing your healthcare benefits. This article explores the key features and advantages that made Plan F so attractive, especially when offered through a trusted organization like AARP. Though no longer available for new beneficiaries, understanding its features can be helpful when considering other Medigap options.

The historical context of Medigap Plan F reveals its significance in providing comprehensive coverage. As healthcare costs continued to rise, Plan F offered peace of mind by covering virtually all out-of-pocket expenses. This made it a popular choice for individuals concerned about unpredictable medical bills. However, changes in Medicare law led to its discontinuation for new enrollees starting in 2020. Those enrolled before this date can keep their Plan F coverage.

The phasing out of Plan F was primarily driven by concerns about its comprehensive coverage potentially encouraging overutilization of healthcare services. The introduction of the Medicare Access and CHIP Reauthorization Act (MACRA) aimed to shift towards more cost-conscious healthcare consumption. While existing Plan F beneficiaries retained their coverage, new enrollees are now directed towards plans like Plan G and Plan N, which require some cost-sharing.

While Plan F is no longer an option for new Medicare beneficiaries, those who enrolled before 2020 can maintain their coverage. This "grandfathered" status allows them to continue enjoying the comprehensive benefits of the plan. For these individuals, understanding the coverage details remains important for managing healthcare expenses effectively.

Those who are newly eligible for Medicare and seeking comprehensive coverage can explore alternative Medigap options, such as Plan G. Plan G offers similar benefits to Plan F, with the exception of the Part B deductible. Comparing available Medigap plans and understanding their coverage is crucial for informed decision-making.

Advantages and Disadvantages of Medicare Supplement Plan F (for existing enrollees)

| Advantages | Disadvantages |

|---|---|

| Predictable out-of-pocket costs | No longer available for new enrollment |

| Comprehensive coverage | Potentially higher premiums compared to other plans |

| No network restrictions |

Best practices for managing your Plan F (for those already enrolled) include reviewing your coverage annually, understanding your benefits and limitations, and communicating any changes in your health status to your insurer.

Frequently Asked Questions:

1. Can I still get Plan F? (No, not if you became eligible for Medicare after January 1, 2020.)

2. What are the alternatives to Plan F? (Plan G and Plan N are popular options.)

3. Does AARP offer other Medicare Supplement plans? (Yes, AARP endorses plans from UnitedHealthcare, including Plan G and Plan N.)

4. What is the difference between Medicare Advantage and Medicare Supplement? (Medicare Advantage is an alternative to Original Medicare, while Medicare Supplement works alongside Original Medicare.)

5. How do I choose the right Medigap plan? (Consider your budget, health needs, and desired level of coverage.)

6. What is the annual open enrollment period for Medigap? (You can make changes to your Medigap plan during the annual Medicare Open Enrollment Period (October 15th to December 7th).)

7. What if I move to a different state? (Your Medigap plan should travel with you, but coverage and premiums might vary.)

8. How can I find more information about Medicare? (You can visit the official Medicare website, Medicare.gov.)

Tips for managing your Medicare Supplement Plan F (if you already have it): Keep your policy information organized, understand your rights as a beneficiary, and stay informed about any changes to Medicare regulations.

Choosing the right Medicare Supplement plan is a crucial step in securing your healthcare future. While Medicare Supplement Plan F, especially when endorsed through a trusted organization like AARP, provided comprehensive coverage and peace of mind for many, it’s essential to understand that it’s no longer available to new Medicare beneficiaries. For those already enrolled in Plan F, understanding the benefits and limitations is key to effectively managing healthcare costs. For those newly eligible, exploring alternatives like Plan G and Plan N, and comparing different options available through AARP’s endorsed plans from UnitedHealthcare, is a critical step in securing the coverage that best fits individual needs and budget. Don’t hesitate to consult with a licensed insurance agent or visit the official Medicare website for personalized guidance. Take the time to research and compare, ensuring you make informed decisions about your healthcare coverage.

Conquer your diy projects with behr stain and polyurethane

Nfs heat pc full version download an immersive experience

Conquering the fungus your guide to antifungal pills