Navigating the Terrain of Medicare Part B Costs

In the tapestry of life's later chapters, healthcare emerges as a central theme, a constant hum beneath the melody of daily existence. For many Americans, Medicare Part B, the segment covering outpatient care, becomes an essential thread in this fabric. Yet, understanding the financial nuances of this vital resource can often feel like deciphering an intricate code. What factors influence Medicare Part B premiums? How do these expenses impact retirement planning? These are questions that echo in the minds of many as they navigate the landscape of aging.

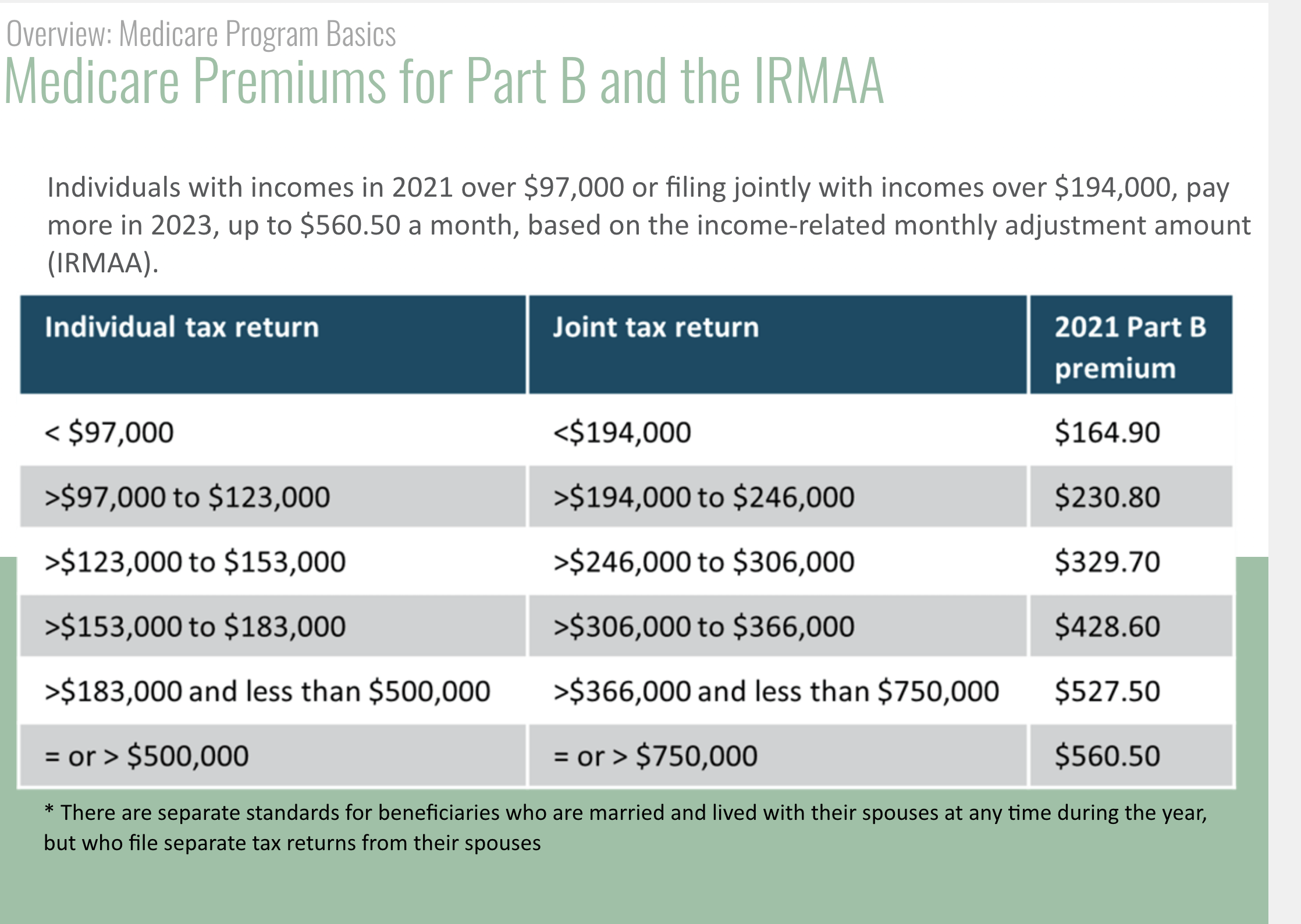

The cost of Medicare Part B is not a monolithic entity but rather a dynamic interplay of various components, each contributing to the overall financial picture. Premiums, the recurring monthly payments, are the most visible aspect of these expenses. But the cost of Medicare Part B extends beyond premiums, encompassing deductibles, coinsurance, and potential out-of-pocket expenses. Grasping the totality of these factors is crucial for informed financial planning and peace of mind.

The genesis of Medicare Part B can be traced back to the Social Security Amendments of 1965, a landmark piece of legislation that fundamentally altered the American healthcare landscape. Born alongside Part A (hospital insurance), Part B was designed to address the growing need for coverage of outpatient medical services. Over the decades, the scope of Part B has evolved, reflecting advancements in medical technology and the changing needs of a growing elderly population. This evolution has also impacted the cost of Medicare Part B, making it a subject of ongoing discussion and debate.

The significance of understanding Medicare Part B pricing cannot be overstated. For retirees living on fixed incomes, these expenses can represent a substantial portion of their monthly budget. Furthermore, the cost of Medicare Part B is not static. It fluctuates annually, influenced by factors such as inflation, healthcare utilization trends, and legislative changes. This inherent variability underscores the importance of staying informed and adapting financial strategies accordingly.

Navigating the complexities of Medicare Part B pricing can feel daunting, yet it is an essential undertaking for securing financial well-being in retirement. Equipping oneself with knowledge about the various components of Part B expenses, understanding the factors that influence these costs, and exploring available resources for assistance are crucial steps in this journey. By delving into the intricacies of Medicare Part B pricing, individuals can empower themselves to make informed decisions and navigate the financial landscape of healthcare with greater confidence.

One simple example is comparing the standard monthly premium for Medicare Part B with the cost of a supplemental Medigap policy. Understanding how these costs interact can help individuals choose the best coverage for their needs and budget.

Advantages and Disadvantages of Medicare Part B Costs

| Advantages | Disadvantages |

|---|---|

| Access to a wide range of outpatient services | Monthly premiums can be substantial for some beneficiaries |

| Predictable cost structure with defined premiums and deductibles | Unexpected medical expenses can still arise due to cost-sharing |

Frequently Asked Questions:

1. What does Medicare Part B cover? Generally, Part B covers doctor visits, outpatient services, preventive care, and some medical equipment.

2. How is the cost of Medicare Part B determined? Premiums are influenced by income, inflation, and healthcare spending trends.

3. Can I appeal my Medicare Part B premium? In certain circumstances, you can appeal if you believe your income was incorrectly assessed.

4. What is the late enrollment penalty for Part B? If you don't enroll when first eligible, you may face a permanent penalty added to your premium.

5. Are there programs to help with Medicare Part B costs? Yes, programs like Extra Help and state assistance programs can provide financial support.

6. How do I estimate my Medicare Part B costs? Use the Medicare.gov online calculators or consult with a financial advisor.

7. Where can I find more information about Medicare Part B costs? Medicare.gov and the Social Security Administration website offer comprehensive resources.

8. When do Medicare Part B premiums typically change? Premiums are usually adjusted annually.

Tips and Tricks: Explore Medigap policies, consider Medicare Advantage plans, and utilize the Medicare Savings Program if eligible.

In conclusion, understanding the cost of Medicare Part B is not merely a financial exercise but an act of self-empowerment. By navigating the intricacies of premiums, deductibles, and cost-sharing, individuals can gain a clearer picture of their healthcare expenses and plan accordingly. The importance of Medicare Part B in securing access to vital outpatient services cannot be overstated. Its benefits extend beyond medical care, offering peace of mind and financial stability in the face of potential health challenges. By actively engaging with the resources available, individuals can take control of their healthcare journey and navigate the complexities of Medicare Part B with confidence and clarity. Take the time to research, ask questions, and seek expert advice. Your informed decisions today can pave the way for a healthier and more secure tomorrow. As we age, the landscape of healthcare can seem daunting, but with knowledge and proactive planning, it becomes a navigable terrain. Medicare Part B, while complex, is a crucial piece of the puzzle, offering a pathway to accessible and affordable care.

Exploring the findlay courier obituary archives

Unleash your inner artist legendary pokemon coloring pages

Thundercloud gray paint disrupting interior design